Understanding Fed Cut Rate: Implications for Long-Term Investment Strategy

October 7, 2025

The well-known investment maxim “don’t fight the Fed” emerged in the 1970s and remains increasingly relevant today. This principle suggests that Federal Reserve monetary policy choices can significantly influence markets and economic conditions, making them crucial considerations for investors. However, maintaining proper perspective requires focusing on the broader trajectory of interest rates rather than individual Fed actions. This perspective proves particularly important as the Fed advances its rate-cutting campaign within a challenging economic landscape.

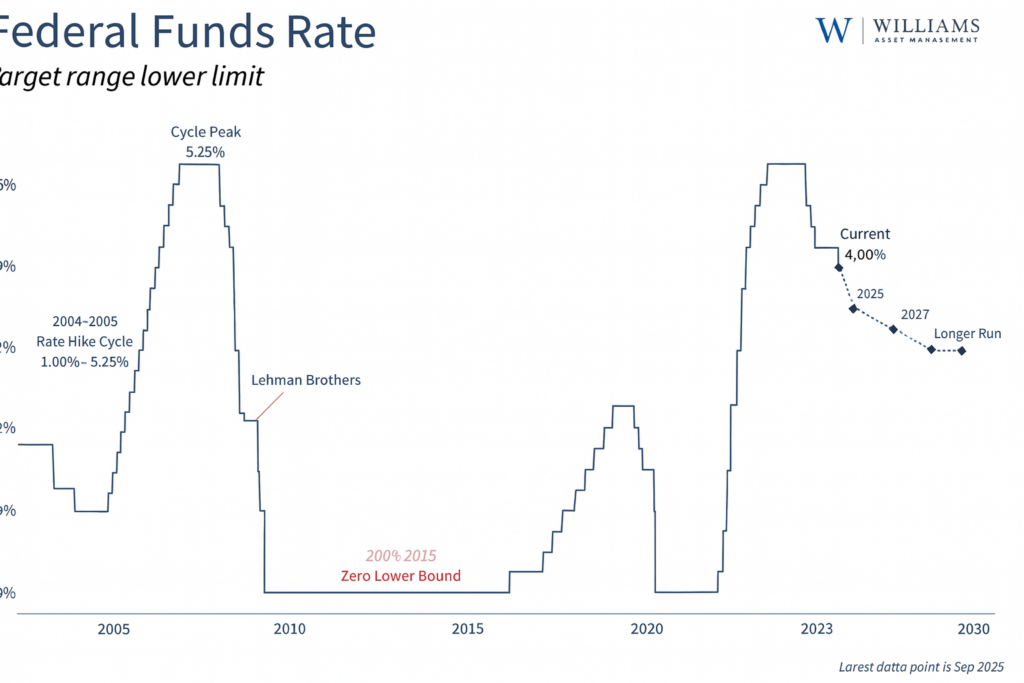

Meeting widespread expectations, the Fed reduced policy rates by 0.25% during its September session, extending the easing phase that commenced in 2024. This action occurred while markets hover near record levels, economic indicators present mixed messages, and questions persist regarding tariffs and inflation pressures. Unlike emergency rate reductions during the 2008 financial crisis or 2020 pandemic, today’s adjustment represents the Fed’s effort to calibrate policy for sustained growth rather than crisis response.

For investors with long-term horizons, comprehending the Fed’s rationale for rate cuts and recognizing how this environment differs from past cycles offers valuable insight for financial planning and portfolio management. Although rate reductions typically benefit financial markets, the essential approach involves maintaining perspective and concentrating on long-term financial objectives rather than reacting excessively to individual policy shifts.

The rationale behind Fed rate cuts carries more weight than timing or magnitude

Fed policymakers examine economic indicators including growth, employment, and inflation when forming their economic outlook. When this outlook becomes unclear, Fed officials and economists naturally hold varying perspectives, creating disagreement about the direction and extent of future rate adjustments. This situation exists today, with substantial variation among officials’ rate projections. While numerous headlines emphasize political tensions between the Fed and the administration, the reality shows this divergence has existed throughout the process.

Amid this disagreement, several key points deserve attention. Initially, the Fed had long anticipated implementing rate cuts. Recent Summary of Economic Projections consistently indicated rate reductions would likely commence this year, though the quantity and size have fluctuated based on tariff developments and market volatility.

Current Fed projections suggest two additional cuts may occur this year, accompanied by an enhanced growth forecast.

Additionally, the recent rate cut differs fundamentally from historical cutting cycles primarily driven by emergencies. Current rate reductions continue reversing the sharp rate increases implemented to combat inflation beginning in 2022. These cuts also occur amid a softening yet positive economic environment, despite potentially weakening employment data and more persistent inflation than anticipated. Put differently, the Fed’s quarter-point rate reduction to guide the economy contrasts sharply with substantial emergency cuts responding to financial system problems or economic crises.

Furthermore, Fed Chair Jerome Powell’s tenure will likely conclude in May 2026. President Trump will appoint the next Fed governor, suggesting the federal funds rate’s most probable trajectory points lower. While short-term interest rates will likely decline accordingly, long-term interest rates respond to market and economic forces rather than Fed policy. For instance, if lower short-term rates stimulated higher inflation, this could inadvertently produce higher long-term rates.

Therefore, while this rate cut continues the Fed’s 2024 trajectory rather than marking a directional change, it demonstrates the Fed’s dedication to supporting economic expansion.

Economic indicators have shown mixed performance recently

Labor market softening primarily influenced the Fed’s decision. The economy generated only 22,000 jobs in August, significantly below projections, with previous months’ figures revised downward substantially. However, the unemployment rate increased modestly to 4.3% due to fewer individuals seeking employment. Again, this differs from previous emergency rate cut periods.

During the 2008 financial crisis, unemployment surged from 5.0% to 10.0%, and in 2020, it leaped from 3.5% to 14.8%. Current employment figures indicate more gradual cooling that may signal softening labor market conditions.

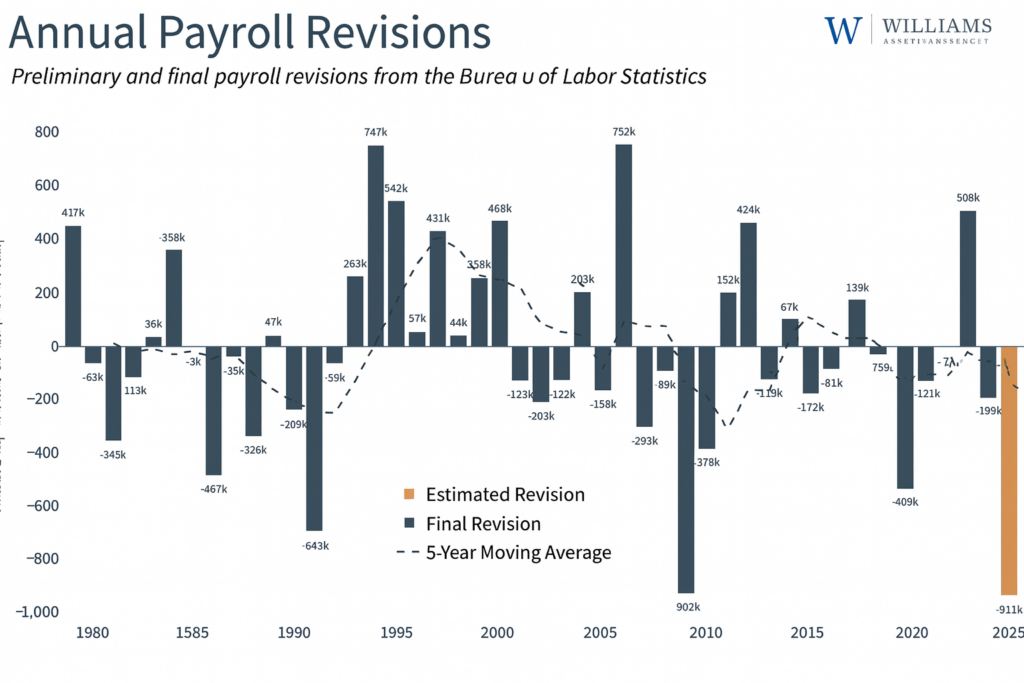

Compounding labor market weakening concerns, recent payroll revisions have revealed a more subdued job growth picture than earlier data suggested. The Bureau of Labor Statistics’ annual revision process indicated 911,000 fewer new positions were created from March 2024 to March 2025, implying the labor market cooled more rapidly than policymakers recognized when making previous monetary policy choices. These preliminary estimates will receive finalization in early 2026.

While weakening labor markets would justify lowering interest rates, the Fed’s inflation concerns support maintaining steady rates, or potentially raising them if tariffs increase prices. The Fed’s preferred inflation measure, the Personal Consumption Expenditures (PCE) Price Index, at 2.6%, remains significantly above the 2% target. Core PCE hovers at 2.9%, while headline and core CPI have stayed persistent at 2.9% and 3.1%, respectively. Earlier inflation progress has not only decelerated, but some trends have reversed in recent months.

The Fed must balance these elements as part of its “dual mandate.” The conflicting signals from these indicators explain disagreement both within the Fed and with the administration. For investors, understanding these patterns will likely prove more valuable for comprehending the economic and interest rate environment than monitoring daily political news.

Rate reductions typically benefit businesses and investors

For investors, the crucial distinction involves whether rate cuts accompany recession or support continued expansion. Although some economic weakness indicators exist, recession signs have not yet emerged. Under these circumstances, rate cuts usually provide widespread benefits across financial markets. Reduced borrowing costs enable companies to finance growth more affordably and decrease debt service costs. Consumer spending may increase if mortgage and credit card rates fall, enhancing demand for goods and services.

One concern regarding today’s rate cuts involves the stock market’s proximity to record highs. While atypical, historical precedents exist. For example, under Alan Greenspan, the Fed reduced rates three times in 1995 and 1996, describing the cuts as “insurance” against economic slowdown. The Fed also implemented cuts in 2019 at market peaks to address global growth concerns. At the recent press conference, Powell characterized this latest policy decision as “a risk management cut” based on the Fed’s assessment that “downside risks to employment have risen.”

For portfolios, history demonstrates that rate cut effects are generally positive across asset classes. While past performance doesn’t guarantee future results, stocks typically benefit as lower rates reduce the discount rate for future earnings and enhance corporate profitability, particularly among growth-focused businesses. Meanwhile, bonds typically gain value due to their higher rates, though this varies across bond sectors and maturities. Conversely, cash will likely experience reduced yields, making it less attractive compared to investments like stocks and bonds.

While each economic cycle presents unique characteristics, navigating policy changes represents a normal aspect of investing. Importantly, rate cuts generally support long-term investors, although balancing risk and reward requires comprehensive understanding of market trends.

The bottom line? The Fed’s recent rate cut may provide economic support amid conflicting signals. Investors should preserve a long-term outlook, emphasizing overall market trends rather than individual Fed decisions.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Advisory services offered through Commonwealth Financial Network®, a Registered Investment Adviser.