Alternative Investments: Risk or Savior?

February 5, 2019

We all know it’s natural for the market to go up and down. But when you have hard-earned cash invested in that market, those ups and downs can sometimes weigh heavily on your emotions. The downs can cause stress, self-doubt, and more importantly, a smaller investment account. While the ups can sometimes make you feel smart, wealthy, and confident. The successful investor knows how to handle his or her emotions when dealing with a prolonged bull market or when the inevitable happens and she is stuck in what seems like a never-ending bear market.

Risk is a nebulous term; it means different things to each person. Many times, the risk is defined by how much a portfolio has in equities. For example, a “moderate risk portfolio” would typically be associated with the 60/40 rule of investing. That is a portfolio with 60%stocks and 40%bonds. That rule-of-thumb has been in existence since Williams Asset Management was established over twenty years ago. This status quo strategy of investing has begun to evolve in the past few years to include alternatives to stocks and bonds.

After the tremendous volatility over the past fifteen years, investors and financial advisors have sought alternative strategies, beyond stocks and bonds, to generate a return and help mitigate risk. The simplest definition of alternative investments are those that are not stocks, bonds, or cash. They include some names that are probably familiar in concept. Products such as real estate, currency, commodities, and private equity. However, alternatives can also be strategies (as opposed to products) such as long/short, market neutral, event-driven, and managed futures. In the past, alternative investments were only available to institutional, accredited, qualified and high-net-worth investors due to their complexity, limited regulations, and lack of liquidity. However, in the past five years or so, alternative investments have been created by mutual fund companies which have brought them to the Main Street investors, not just Wall Street investors.

With the use of this blog, we hope to educate you about the benefits of alternative investments. In our opinion, the main reason investors should consider alternatives in their portfolio is to potentially reduce risk. In the past 15 years or so, correlations in stocks, bonds, and other investments have increased. Said another way, in general, investments are increasing and decreasing at the same time. Over the same 15 years, many alternative investment correlations with traditional asset classes have decreased. Unfortunately, many investors either don’t understand alternatives or they have a negative stigma due to the complex names like merger arbitrage or hedge fund. A common belief among misinformed investors and financial advisors is that they feel that alternative investments carry far more risk than other investments. On the contrary, they have the potential to reduce the overall risk of your portfolio. When non-correlated investments are included in a portfolio, you have the potential to decrease risk and potentially not sacrifice returns. They do this by not following the same up and down patterns as stocks and bonds. So when your stock and bond investments fall in value, the alternative investments can potentially follow the same path and could improve your portfolio’s overall performance.

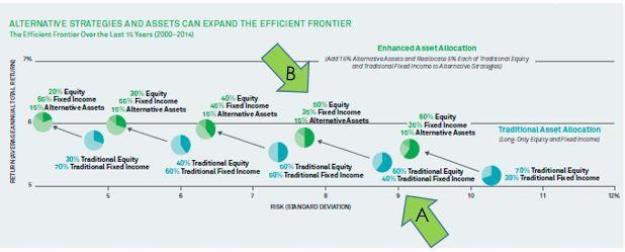

The chart below shows how adding alternative assets to a traditional stock/bond portfolio would have simultaneously reduced risk and increased returns.

Investing involves risk including possible loss of principal. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Sources: BlackRock; Informa Investment Solutions. Equity is represented by the S&P 500 Index. Fixed Income is represented by the Barclays US Aggregate Bond Index. Enhanced portfolios include a 15% allocation to alternative assets, a 5% allocation to alternative equity strategies within the equity allocation and a 5% allocation to alternative fixed income strategies within the fixed income allocation. To fund these additional allocations, the equity allocation of each traditional portfolio is reduced by 15% and the fixed income allocation is reduced by 10%. The 15% allocation to alternative assets is represented by a 5% allocation to the Goldman Sachs Commodity Index, a 5% allocation to the Barclay Currency Traders Index and a 5% allocation to the NAREIT Equity Index. The 5% allocation to alternative equity strategies is represented by the Dow Jones/Credit Suisse Long Short Equity Index. The 5% allocation to alternative fixed income strategies is represented by the Dow Jones/Credit Suisse Fixed Income Arbitrage Index.

In this hypothetical, you start with a traditional 60/40 portfolio (A) and reallocate 15% of your portfolio to alternative assets, such as commodities and currency (B). The result is a significant change over this long time frame of 14 years. You would have reduced your risk and increased your returns. There are two important points to remember if you decide to add alternatives to your portfolio. First, you need to be patient. There will be periods of time, possibly years in length, where equities perform well and some alternatives do not. This is the reality of having non-correlating investments in your portfolio. Second, alternative investments require much more due diligence then the typical equity-oriented mutual fund. You need to be prepared to put in the time to sort through the choices available to find the appropriate investment for you and your portfolio.

So, what’s the answer? Are alternatives a risk or a savior? We believe they are a savior and hopefully, you do too.

To find out more about alternative investments and how they fit into a portfolio, read Chapter 8 of The Art of Retirement, written by Gary Williams.

*Investing in alternative investments may not be suitable for all investors and involves special risks, such as risk associated with leveraging the investment, adverse market forces, regulatory changes, and illiquidity. There is no assurance that the investment objective will be attained.